Safe-Haven Liquidation Paradox: Margin-Call Transmission Architecture

Deconstruct forced-selling from oil shock to gold liquidation. Recognize margin contagion as structural architecture.

“Insights age like wine; news ages like milk. The evidence below is a timestamp of a recurring cycle. Observe the mechanism before it repeats.”

🎧 Listen at 08:30 EDT

1. Eternal Logic

Core Thesis

Supply shocks produce a paradox. Safe-havens decline during peak risk. This is structural. Energy spikes breach risk budgets. Margin calls force liquidation by liquidity rank. Gold, the most liquid asset, becomes the first target.

Operating Mechanism

Stages execute sequentially. A chokepoint removes supply. Energy futures reprice, expanding losses. Margin thresholds breach, triggering forced sales. Gold absorbs selling as the fastest asset. Dollar strengthens, adding pressure. The diagnostic: gold decline minus dollar-implied move. Excess magnitude measures intensity.

Systemic Conclusion

Past margin breach, the reaction is deterministic. Managers sell by liquidity rank. Gold selling triggers secondary calls on gold-collateralized positions. The loop terminates only via central bank liquidity. Until then, safe havens behave as risk.

2. The 2026-04-13 Case Study: Empirical Proof

Trigger

The US announced a Hormuz Strait blockade after talks collapsed. WTI surged +6.95% to $103.28. Brent reached $95.2. The chokepoint targeted global oil transit. VIX expanded +10.61% to 21.27 during the global session.

Transmission

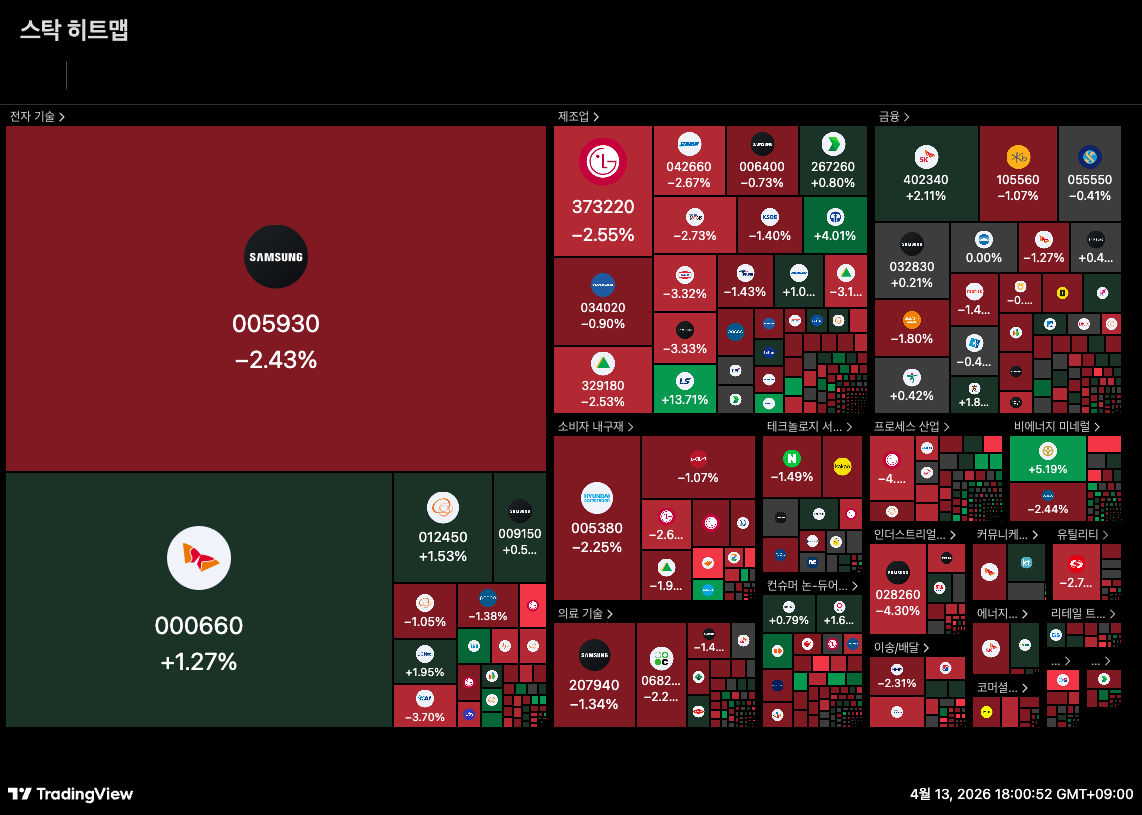

Four layers repriced within 12 hours. The Korean unit weakened to 1,488.7 per dollar. KOSPI declined -0.86% on $780M foreign and institutional selling. DXY stood at 98.7. Gold fell -0.92% despite peak stress. On the KRX, foreign KOSPI selling totaled $309M. SK Hynix absorbed $306M net buying. Samsung Electronics drew $261M in short-selling at a 5.95% ratio. Energy and defense flows decoupled from the index.

Evidence

Gold’s -0.92% decline exceeded the dollar-implied range by over 2x. VIX rising with gold falling matches 2020 and 2008 margin-call liquidation patterns. SOXX put/call ratio stood at 1.96. SOX closed at 8,889.8 (+2.31%). US10Y yield reached 4.336%. GS 1Q26 EPS consensus 15.92 is positioned as the binary regime classifier. NQ futures settled at 25,111 (-0.67%), near the Asia session low of 25,061.

Outcome

A three-layer regime formed. Macro premium dominated index pricing. Sector decoupling activated for AI/HBM. The gold-VIX divergence left the systemic liquidity state unresolved pending GS confirmation.

3. The Structural Filter: Identifying the Mechanism Across Cycles

Filter 1: Excess Gold Decline Ratio

If gold declines >1.5x the dollar-implied move during a shock, margin-call liquidation is active. Dollar move equals DXY change times gold beta. VIX >20 confirms.

Filter 2: Intra-Sector Flow Divergence

If index selling is offset by single-name buying at ratio >0.8, the state is Selective Rotation. Below 0.5, conviction collapses into Broad Liquidation.

Filter 3: Intermediary Revenue Classifier

FICC revenue classifies the regime. Beat confirms intermediaries profit: Rotation. Miss confirms volatility exceeds capacity: Liquidation. Invalidation: VIX >30 for 5+ sessions erodes market-making margins.

4. Regime Dynamics: The Lifecycle of the Mechanism

Regime Persistence

Energy costs compress margins, expanding losses and margin pressure. Dollar strength burdens non-dollar economies, accelerating outflows that strengthen dollar further. Gold liquidation triggers secondary calls. Physical chokepoints resist resolution.

Regime Exhaustion

Dollar strength triggers demand destruction, capping the price spiral. FICC revenue inverts: past the volatility threshold, counterparty risk converts trading profits into losses. Entropy mounts.

Archival End-State

Chokepoint removal collapses risk premium. Or volatility forces central bank liquidity. The mechanism archives, re-emerging at the next leverage peak.

This content is for informational and educational purposes only and does not constitute financial, investment, tax, or legal advice. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. Consult a qualified advisor before investing. Author may hold positions in discussed securities.

Access Archive: Empirical Validation