Partial Risk Premium Compression: The Architecture of a Self-Verifying Conditional Equity Regime

Separate Currency from Conviction. The Flat Instrument Holds Both Endpoints of the Regime.

“Insights age like wine; news ages like milk. The evidence below is a timestamp of a recurring cycle. Observe the mechanism before it repeats.”

🎧 Listen at 08:30 EDT

1. Eternal Logic

Core Thesis

Three instruments, observed simultaneously, identify the structural source of any equity rally. They are the equity index, the rate futures market, and the cross-asset pair of implied volatility and gold. When equities rise, rate futures stay flat, VIX does not decline, and gold rises, these outputs share one explanatory mechanism. The gain originated from partial risk premium compression, incomplete because the triggering event remained unresolved. Historically, this configuration is associated with higher full-reversal rates than monetary-policy-anchored sessions, and it is falsifiable in real time.

Operating Mechanism

The diagnostic rests on structural logic applied across independent channels. Monetary policy channel rallies require rate futures to decline. Rate futures did not move. The monetary policy channel is excluded. Conviction rallies compress VIX. VIX, the currency-independent test for conviction, did not decline. The conviction channel is excluded. The remaining mechanism is risk premium compression. A specific uncertainty was partially reduced, requiring investors to accept less compensation for holding risk assets. Gold rose for two concurrent reasons. Residual uncertainty persisted because the event remained unresolved. Dollar weakness independently amplified gold prices denominated in USD. No Positive Feedback Loop anchored the repricing to improved fundamental cash flows.

Systemic Conclusion

This mechanism generates its own verification test. The Internal Contradiction is structural. If the triggering event fails, the premium reinstates and equity gains reverse without residual. If the event resolves permanently, dollar stability returns and rate futures begin declining as inflation expectations fall. Either path produces an unambiguous next confirmation point, which defines the mechanism’s primary analytical utility.

2. The 2026-05-07 Case Study: Empirical Proof

Trigger

On May 7, 2026, markets priced an accelerating probability of a US-Iran ceasefire, activating two parallel transmission channels. The direct channel partially compressed war-related risk premium from global asset prices. The financial conditions channel propagated through energy markets into inflation expectations and bond yields. The triggering event remained unresolved at session close.

Transmission

Brent crude fell 8.60% in a single session, consistent with a war risk premium unwinding from the forward energy curve rather than a fundamental supply or demand shift. The oil decline lowered inflation expectations, pulling US 10-year Treasury yields down 7.8 basis points to 4.347%. The US Dollar Index declined 0.5%, reflecting receding safe-haven demand as war risk compressed. The two primary channels operated independently and concurrently. Capital rotated into Doosan Enerbility (nuclear power generation equipment for US, Middle Eastern, and European projects), Taihan Fiberoptics (optical cable for North American hyperscale datacenter networks), and Seojin System (ESS and power modules for US grid infrastructure), documenting specific sectoral implications of the ceasefire narrative rather than broad market participation.

Evidence

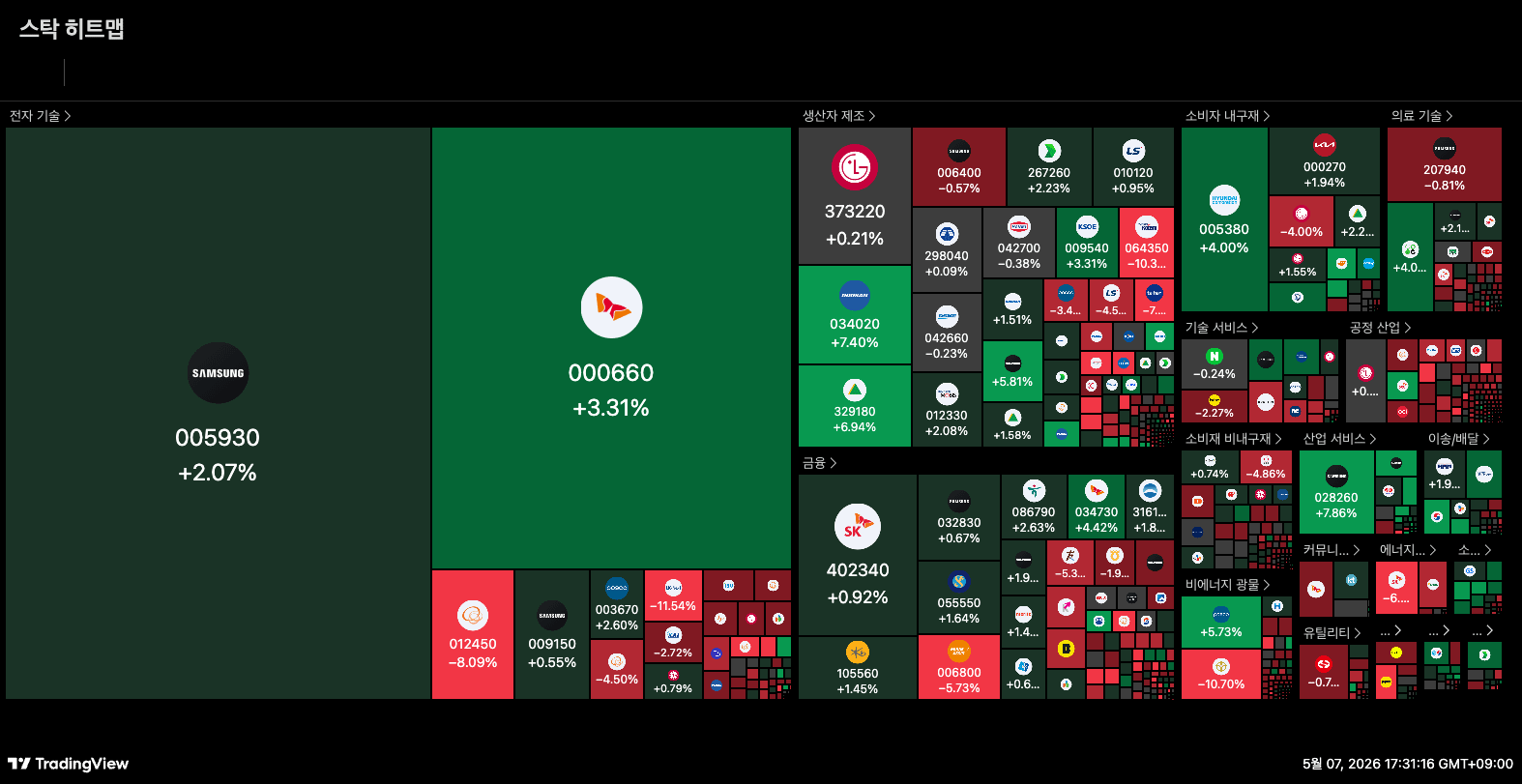

KOSPI closed at 7,490.05, gaining 1.43%. KOSPI 200 futures gained 2.39%, outperforming the cash index. Large-cap stocks gained 1.6%, mid-cap declined 0.3%, and small-cap declined 0.5%. At 5:00 AM EDT, Nasdaq 100 futures registered +0.09% and S&P 500 futures registered +0.10%. The 30-Day Fed Funds and SOFR futures registered zero basis point change at 5:00 AM EDT. The US Dollar Index declined 0.5%. Gold gained 0.92% to 4,737.49, reflecting residual ceasefire uncertainty and dollar weakness amplifying USD-denominated prices. VIX gained 0.58% to 17.49. As the currency-independent instrument, VIX’s failure to decline confirms conviction-based risk-on did not drive the session. HD Hyundai Heavy Industries recorded a short-selling transaction ratio of 11.44% in a session where its price gained 6.94%, consistent with the conditional positioning signaled by VIX.

Outcome

Zero basis point movement in both Fed Funds and SOFR futures at 5:00 AM EDT confirms the monetary policy channel contributed 0% to the repricing. VIX rising alongside equities confirms the conviction channel contributed 0%. VIX rising rather than declining further confirms the compression was partial, as complete resolution would have produced VIX compression alongside equity gains. The session gain originated from partial risk premium compression. The ceasefire remained unresolved. The equilibrium is conditionally stable and carries full reversal risk. If the event fails, the premium reinstates and session gains reverse. If the event resolves permanently, Fed Funds futures begin declining and the regime reclassifies.

3. The Structural Filter: Identifying the Mechanism Across Cycles

Filter 1: The Rate Futures Divergence

When equities gain materially and rate futures show no directional movement, the monetary policy channel is excluded. When VIX rises rather than declining, the conviction-based channel is also excluded. VIX is the primary conviction test because it carries no currency channel confound. Gold requires decomposition into geopolitical and currency components before classification. The configuration documents partial risk premium compression with the underlying event unresolved.

Filter 2: The Flow Distribution Test

When large-scale institutional selling concentrates in a narrow set of positions while the same participants simultaneously buy thematically distinct assets, the activity documents regime rotation rather than capital withdrawal. Broad macro exit distributes selling without sectoral differentiation. Concentrated selling is a positioning decision, making it consistent with the risk premium compression hypothesis rather than contradictory to it.

Filter 3: The Regime Transformation Signal

The regime transformation signal arrives through the same instrument that produced the original diagnostic. When rate futures begin declining following a risk premium compression event, the event has propagated into monetary policy expectations and the regime reclassifies. This is simultaneously the Invalidation Point for the original risk premium classification.

4. Regime Dynamics: The Lifecycle of the Mechanism

Regime Persistence

The risk premium compression regime persists through structural suspension, not through a Positive Feedback Loop. Regime Persistence is maintained by the continuous absence of contradicting signals, not by constructive structural development. Without monetary policy repricing, the gain lacks structural anchoring. Dollar weakness and residual uncertainty sustain gold at elevated levels, confirming the compression remains incomplete.

Regime Exhaustion

The Internal Contradiction is structurally deterministic. A system built on a single uncertainty’s partial reduction contains no self-reinforcing mechanism. Systemic Exhaustion arrives through one of two endpoints. Event failure reinstates the full premium and reverses all gains. Permanent resolution activates the financial conditions channel and initiates rate futures movement. Neither is gradual.

Archival End-State

The terminal state arrives at the moment of transformation, not of price movement. Event failure returns the system to pre-event equilibrium with zero structural change. Permanent resolution reclassifies the regime from risk premium to monetary policy channel, transforming participant logic from event-contingent to rate-expectation based. Regime Inversion completes when the instrument that registered zero movement begins declining. The same tool that identified the regime’s origin identifies its termination.

“This content is for informational and educational purposes only and does not constitute financial, investment, tax, or legal advice. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. Consult a qualified advisor before investing. Author may hold positions in discussed securities.”

Access Archive: Empirical Validation