Dual-Function Catalyst: The Liquidity Bridge Architecture

Isolate the exit mechanism from the directional signal. Reclassify the catalyst first.

“Insights age like wine; news ages like milk. The evidence below is a timestamp of a recurring cycle. Observe the mechanism before it repeats.”

🎧Listen at 08:30 EDT

1. Eternal Logic

Core Thesis

A single catalyst that activates price appreciation in a sold asset creates exit liquidity for sellers and entry rationale for buyers at the same time. This dual function classifies the catalyst as a liquidity bridge, not a directional signal.

Operating Mechanism

The mechanism operates in five steps. A catalyst provides institutional buyers with the rationale to enter at depressed price levels. That institutional buying produces price appreciation in the target name. The appreciation creates the exit price disposing participants need to reduce large positions without forced liquidation. Domestic capital absorbs the disposal flow and defends the index. Foreign capital completes sector redeployment into designated allocations within the same session. Each step depends on the prior one. The mechanism fails when the catalyst is absent or appreciation is insufficient to satisfy both participant objectives.

Systemic Conclusion

The forced reaction is index defense by domestic capital while foreign capital executes undisrupted redeployment. The defining confirmation is the absence of forced liquidation. When this condition is present, redeployment is the operative state.

2. The 2026-05-18 Case Study: Empirical Proof

Trigger

A global bond shock drove US10Y to 4.592%, pushed US30Y above 5.10%, elevated MOVE 14.71%, and placed CME FedWatch rate hike probability at 49.4%. SOX declined 4.02% on May 15 as a semiconductor sector leading signal. These inputs raised discount rates for Korean high-valuation sectors and triggered a KOSPI intraday decline of 4.5%, activating a sidecar. The sidecar-level price compression created the depressed entry conditions that institutional buyers require to act on a qualifying catalyst. Two Korea-specific catalysts then emerged within the same session.

Transmission

A Seoul court granted a partial injunction protecting Samsung Electronics production continuity, imposing a penalty of 100 million KRW per day for violations. Nomura raised its Samsung Electronics target price from 340,000 KRW to 590,000 KRW, a 73.5% increase. Nomura also raised its SK Hynix target from 2,340,000 KRW to 4,000,000 KRW, a 70.9% increase. These catalysts activated securities firm buying at depressed price levels and drove Samsung Electronics and SK Hynix into price appreciation. That appreciation provided the exit price foreign investors needed to process 2.2614 trillion KRW in combined disposals within a single session. Foreign capital simultaneously exited semiconductor majors and reallocated across domestic non-semiconductor sectors and within the semiconductor supply chain by process stage.

Evidence

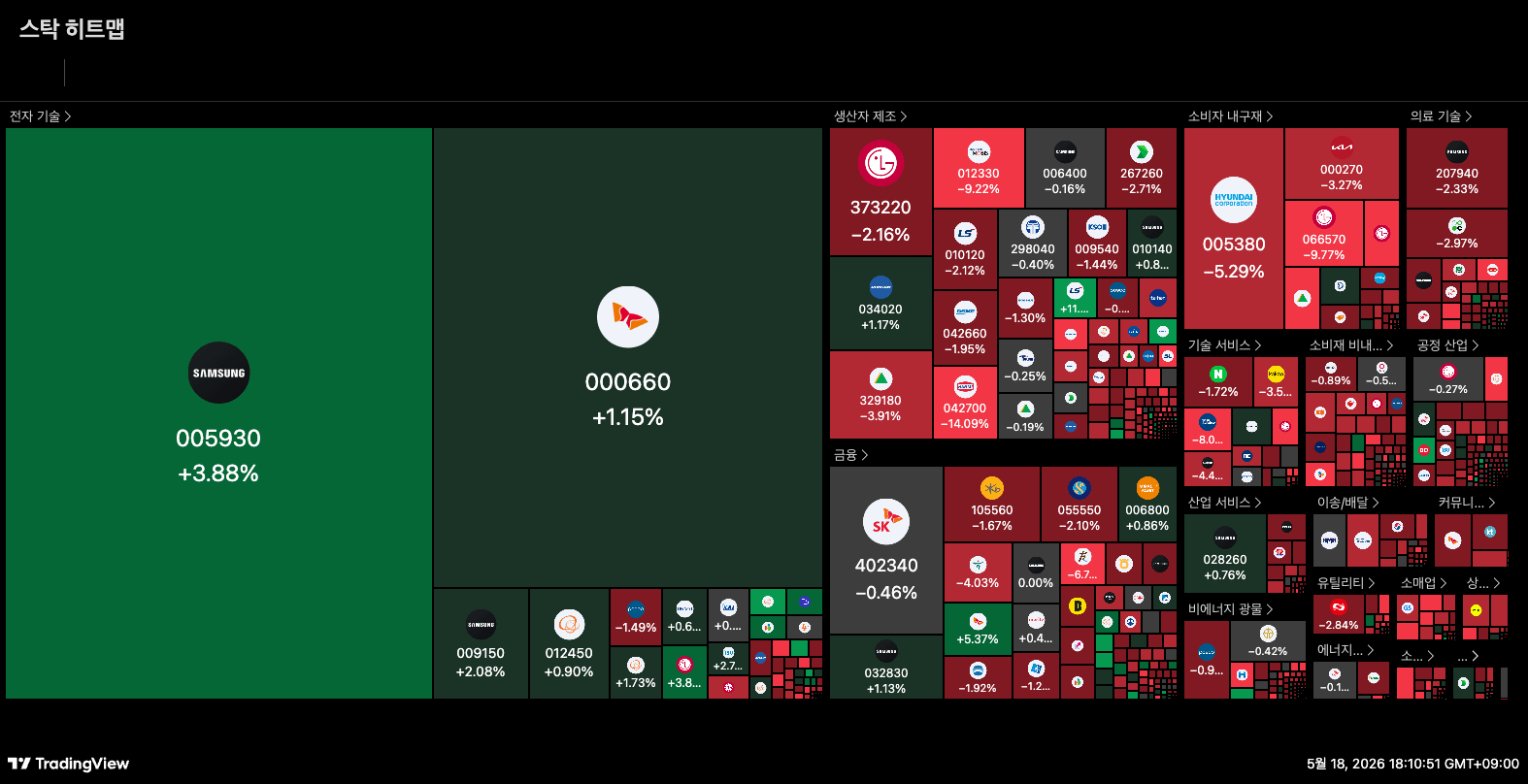

Samsung Electronics closed at +3.88% while foreign investors executed 1.2402 trillion KRW in net disposals within the same session, confirming counter-directional selling during price appreciation. SK Hynix closed at +1.15% against 1.0211 trillion KRW in foreign net selling. No margin calls or forced liquidations were reported, classifying this as a strategic positioning adjustment rather than a stress event. VIX stood at 18.95, below the 20 threshold, confirming elevated rate shock rather than systemic stress as the operative regime. LG Electronics fell 9.77% with 186.7 billion KRW in net foreign selling. Hyundai Mobis fell 9.22% with 158.8 billion KRW. Hyundai Motor fell 5.29% with 135.6 billion KRW. All three operated under identical foreign selling conditions without a recovery catalyst. The absence of a comparable catalyst isolates Samsung’s rebound as catalyst-dependent and eliminates a broad market recovery explanation. Among identified domestic sector destinations, foreign capital distributed to construction at 67.3 billion KRW, power infrastructure at 62.7 billion KRW, secondary batteries at 82.2 billion KRW, and insurance at 36.9 billion KRW. Within the semiconductor supply chain, foreign positioning separated by process stage. Jusung Engineering, a front-end ALD and CVD equipment provider, closed at +29.96% as the KOSDAQ top foreign net buy at 38.08 billion KRW. Hanmi Semiconductor, a specialist in HBM TC bonding (a thermal compression die-stacking process specific to HBM assembly), closed at -14.09% with 137.5 billion KRW in net foreign selling and a short selling ratio of 13.94%.

Outcome

KOSPI closed at +0.31%, recovering from its intraday sidecar low. Individual investors provided 2.2093 trillion KRW in absorption across eight consecutive sessions. Securities firms contributed 1.4002 trillion KRW on an event-driven basis. Combined with additional institutional categories, total domestic absorption of 3.6519 trillion KRW matched aggregate foreign net selling. 72.6% of listed stocks closed lower. U.S. counterpart validation from Eaton, Vertiv, AMAT, and LRCX for the power infrastructure and HBM front-end redeployment signal remains open at this session’s close.

3. The Structural Filter: Identifying the Mechanism Across Cycles

Filter 1: Rate Shock Regime with Sub-20 VIX

If VIX stands below 20 and a major index records an intraday decline exceeding 3% alongside a session-level circuit breaker activation, the rate shock regime condition is met. The required confirmation is the absence of margin calls and forced liquidations. Counter-directional foreign selling during price appreciation is a redeployment signal in this environment.

Filter 2: Counter-Directional Selling Pattern

If a major index constituent closes with a positive return while foreign investors execute net selling in that constituent within the same session, the price movement is not a directional signal. The operative mechanism is exit liquidity generation. If the constituent declines while foreign investors sell, the classification shifts to forced liquidation and the redeployment signal is suspended. The required condition is that counter-directional selling occurs during price appreciation, not during decline.

Filter 3: Intra-Sector Process-Level Positioning Split

If foreign investors execute simultaneous net selling in one supply chain process stage and net buying in another within the same session and within the same end market, the redeployment is classified as process-level rotation rather than sector exit. The operative signal is directional divergence between two components of the same supply chain. If both process stages move in the same direction within the session, the signal is reclassified as broad sector liquidation and the process-level rotation thesis is invalid. The Invalidation Point is the absence of any directional divergence across supply chain process stages within the identified sector.

4. Regime Dynamics: The Lifecycle of the Mechanism

Regime Persistence

The Positive Feedback Loop sustaining the mechanism depends on two parallel conditions. Domestic retail capital maintains sufficient depth to absorb large-scale foreign disposal flows without triggering index deterioration. Domestic institutional capital retains the capacity to respond to event-driven catalysts at speed. These two conditions reinforce each other. Retail depth prevents price collapse, which preserves institutional confidence in catalyst-driven entry rationale. As long as both conditions hold, Regime Persistence continues and foreign capital executes redeployment without forced liquidation disrupting the absorption structure.

Regime Exhaustion

The Internal Contradiction within the mechanism is the finite capacity of domestic absorbers. Retail accumulation across consecutive sessions depletes available dry powder at the individual investor level, and the unrealized losses accumulated on those positions become the direct input for a secondary failure mode. Institutional capacity is restricted to sessions with a qualifying catalyst. If macro shock intensity reaches the threshold where discount rate pressure converts those accumulated unrealized losses into margin call events, the absorber base transitions from a stabilizing force to a liquidating force. Systemic Exhaustion occurs when the cost of maintaining domestic absorption exceeds the marginal utility of index defense. The observable signal is retail-level margin call activity concurrent with ongoing foreign disposal flows.

Archival End-State

Regime Inversion occurs when domestic absorption capacity collapses and foreign redeployment loses its execution environment. The structural reclassification is confirmed when counter-directional selling during price appreciation is replaced by concurrent directional selling during price decline across multiple sessions. At that point, the liquidity bridge mechanism ceases to function and the market transitions into a stress-driven liquidation regime. The Archival End-State is the dissolution of the full transmission structure connecting domestic index defense through sector redeployment to cross-market validation in U.S. counterpart names. Its dissolution terminates the environment that made undisrupted single-session redeployment possible.

This content is for informational and educational purposes only and does not constitute financial, investment, tax, or legal advice. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. Consult a qualified advisor before investing. Author may hold positions in discussed securities.

Access Archive: Empirical Validation