Concentration Liquidation Cascade: The Architecture of Amplified Exit

Diagnose the mechanism. Separate position rebalancing from structural collapse.

“Insights age like wine; news ages like milk. The evidence below is a timestamp of a recurring cycle. Observe the mechanism before it repeats.”

🎧Listen at 08:30 EDT

1. Eternal Logic

Core Thesis

When two index-dominant names function as proxies for a macro thesis, thesis inversion generates liquidation pressure proportional to their combined index weight. The visible output is a broad market drawdown. The actual input is a two-position liquidation event. The structural invariant is that position concentration amplifies an exit beyond its original scale. A two-position exit transmits as a market-wide event because those positions carry index weight that exceeds their fundamental size. Diagnostic precision requires identifying the source of the exit before assigning structural meaning to the drawdown.

Operating Mechanism

Capital concentration creates hidden leverage. When two names carry the majority weight of a macro thesis, their combined influence on index-linked instruments exceeds their fundamental allocation. Any forced exit does not remain isolated within those two positions. The decline propagates through the index itself, because index-linked instruments must rebalance against the weight change. The exit type is confirmed by the short selling ratio relative to the market average. A short selling ratio significantly below the market average during a major decline identifies the holder base as long-only institutional capital, not speculative positions. Long-only liquidation requires no borrowing mechanism. It activates the moment the thesis loses its logical basis. The resulting index decline triggers non-arbitrage program selling. Program selling is a mechanical transmission layer. It does not create a directional signal. It amplifies the existing signal from the concentrated exit and distributes it across the full index.

Systemic Conclusion

The forced reaction follows a fixed sequence. Concentrated real selling depresses the index-dominant names. Index decline triggers program selling. Program selling transmits that decline mechanically across all sectors, regardless of their individual fundamentals. The final drawdown reflects amplified transmission, not independent sector deterioration. Systemic Exhaustion occurs when an opposing capital force absorbs the liquidation at scale. Partial index recovery from session lows confirms the amplification was artificial. The underlying signal was more contained than the final drawdown suggested.

2. The 2026-05-15 Case Study: Empirical Proof

Trigger

The U.S.-China summit failed to deliver specific commitments on semiconductor supply chain normalization or tariff structures. A hawkish Trump statement on Iran reached Korean markets as KOSPI formed its intraday high of 8,046.78. The convergence of both catalysts invalidated the 8,000-point rally thesis at the moment of maximum session optimism. The liquidation mechanism activated immediately.

Transmission

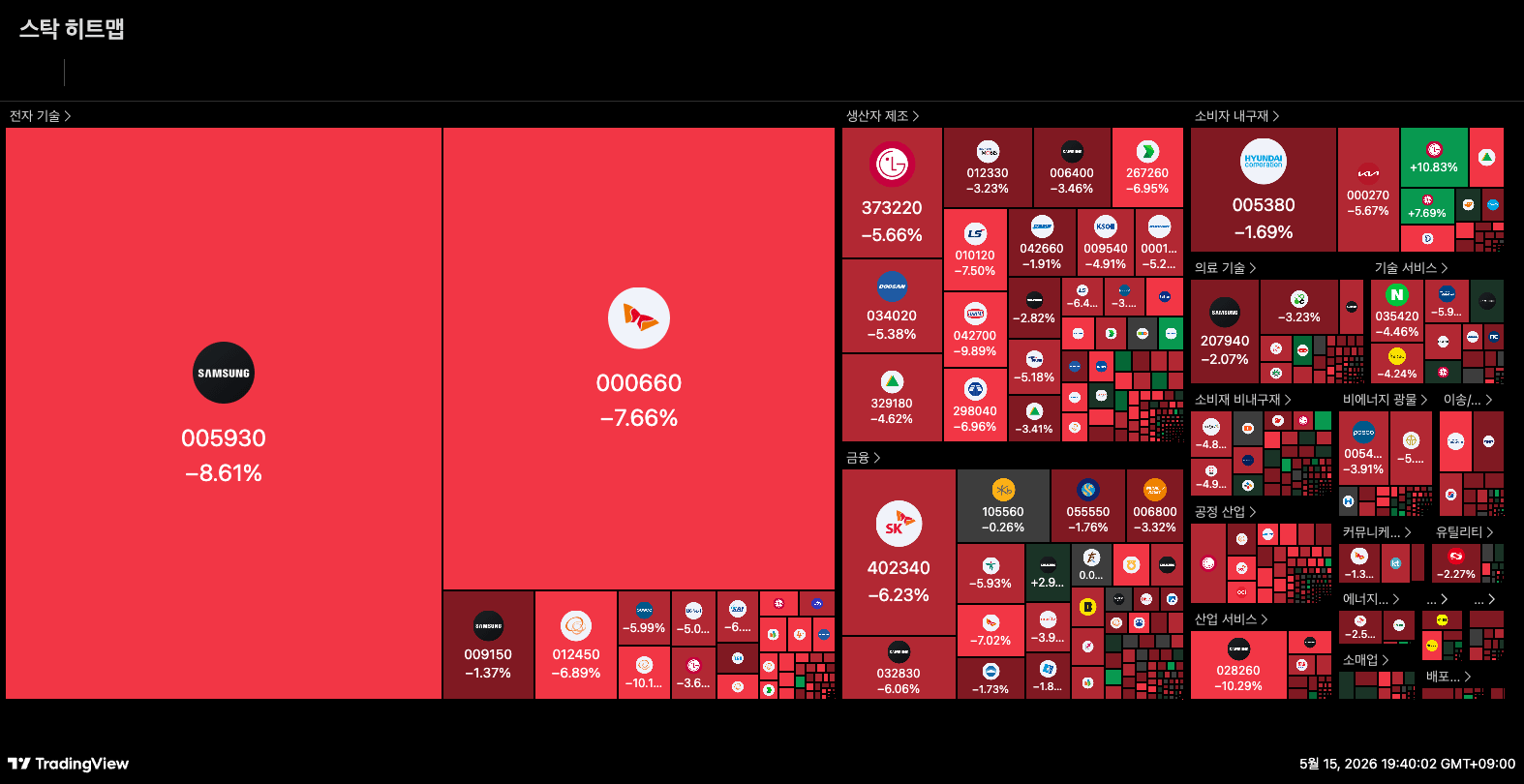

Foreign capital concentrated net selling in Samsung Electronics at 2.50 trillion KRW and SK hynix at 2.64 trillion KRW. The combined outflow of 5.14 trillion KRW represented 90.7% of total foreign KOSPI net outflows of 5.66 trillion KRW. This concentration ratio classified the event as a two-position liquidation, not a market-wide exit. The combined index weight of these two names depressed the KOSPI 200 benchmark. Non-arbitrage program algorithms then calculated a 4.47 trillion KRW sell response. This cascade transmitted the decline mechanically across all sectors regardless of individual sector fundamentals. The sector-wide drawdown was the output of this transmission, not evidence of independent sector deterioration. The intraday decline reached its low of 7,371.68, representing an intraday drawdown of approximately 8% from the session high. Simultaneously, foreign capital directed net buying into Hana Micron at 91.8 billion KRW. Hana Micron is the leading HBM memory packaging supplier in KOSDAQ and reported Q1 earnings above consensus. Foreign capital also directed net buying into AI data center power infrastructure names. LS ELECTRIC received 43.0 billion KRW, Sanil Electric received 40.4 billion KRW, and Taihan Cable and Solution received 46.7 billion KRW. Selling in upstream semiconductor names and simultaneous buying in downstream infrastructure names by the same foreign capital class confirmed a within-supply-chain rotation.

Evidence

Samsung Electronics posted a short selling ratio of 0.71% and SK hynix posted 0.54%, against a market average of 3.07%. Samsung’s ratio was less than one-quarter of the market average. SK hynix’s ratio was less than one-fifth. Both stocks declined 8.61% and 7.66% respectively while maintaining these ratios. Near-zero short ratios confirmed that selling originated from existing long holders, not speculative attacks. This distinction is the primary diagnostic variable for determining the structural character of the session. Individual investors absorbed 7.23 trillion KRW in net buying, covering 97.8% of combined institutional and foreign net selling of 7.40 trillion KRW. Hana Micron’s foreign net buying of 91.8 billion KRW represented 1.8% of the combined Samsung Electronics and SK hynix outflow of 5.13 trillion KRW. This asymmetric scale relationship quantifies the divergence between the rotation signal and the primary exit signal. Gold declined 2.71% as VIX rose 8.34%, confirming DXY at 99.15 as the dominant session variable rather than equity-specific risk. DRAM export prices recorded year-over-year growth of 232.8% in April per the Bank of Korea. This figure confirmed the AI demand cycle remained structurally intact at the time of the decline. The fundamental demand data provided the logical basis for semiconductor supply-demand dynamics to reassert leadership once macro pressure stabilized.

Outcome

KOSPI closed at 7,493.18, a 6.12% decline, recovering 121.5 points from its intraday low of 7,371.68. The recovery confirmed the amplification mechanism had exhausted at scale. The within-supply-chain rotation signal remained structurally conditional pending U.S. session validation.

3. The Structural Filter: Identifying the Mechanism Across Cycles

Filter 1: Concentration Threshold Diagnostic

When the top two names account for more than 80% of total foreign net outflows in a single session, apply the concentration filter first. When both also carry short selling ratios below one-third of the market average, classify the event as a position liquidation, not a market break. The concentration ratio is the primary separator between a structural sector exit and a two-position rebalancing event. Apply this filter before assigning sector-level causation to any single-session drawdown. A market-wide decline driven by two concentrated positions is a position event, not a structural market signal.

Filter 2: Simultaneous Divergence Signal

When foreign capital sells index-dominant upstream names and simultaneously buys adjacent supply chain nodes in the same session, classify the event as a within-supply-chain rotation. The simultaneous presence of both directional signals rules out a panic exit interpretation. A panic exit does not concentrate new capital into adjacent nodes of the same supply chain. A rotation does. The divergence between the exit point and the entry point within the same session, executed by the same capital class, is the core diagnostic variable. Uniform directional outflow across all nodes indicates a sector exit. Divergent flow confirms a rotation.

Filter 3: Program Cascade Invalidation Point

When mechanical program selling accounts for more than 75% of the total index drawdown, strip the amplification effect and read the underlying directional signal independently. The invalidation point for any rotation signal derived from this framework is DXY above 100 or the 10-year yield above 4.6%. When either threshold is breached, the EM capital exit framework becomes the dominant analytical lens. The rotation signal loses analytical validity regardless of the session-level supply chain evidence.

4. Regime Dynamics: The Lifecycle of the Mechanism

Regime Persistence

The positive feedback loop sustaining this mechanism operates on structural demand data. When sector-level data confirms a multi-year growth trajectory, institutional capital concentrates in the names with the highest direct revenue exposure. This concentration increases their index weight. Higher index weight amplifies their influence on index-linked instruments. Amplified influence attracts additional capital seeking index-correlated returns. Additional capital reinforces the original concentration. Regime Persistence continues as long as structural demand data remains intact and no macro-regime variable inverts the risk tolerance of the dominant holding class.

Regime Exhaustion

The internal contradiction within this architecture is mathematical. Concentration beyond a threshold makes orderly liquidation structurally impossible. Position size relative to daily market liquidity means that any forced exit produces index-level amplification regardless of the exit’s scale. Each amplification event reduces the holding class’s confidence in the concentration structure. Confidence reduction produces partial liquidation. Partial liquidation produces further amplification. The positive feedback loop inverts into a destructive one. Systemic Exhaustion occurs when the amplification mechanism itself becomes the primary source of session volatility, displacing external macro catalysts as the dominant driver.

Archival End-State

Regime Inversion terminates when institutional capital reclassifies its allocation logic from index-beta concentration to supply-chain-node precision selection. This reclassification appears in data as a persistent divergence between top-index-weight names and adjacent supply chain components. When adjacent nodes consistently outperform dominant names across multiple sessions without reverting to the prior concentration pattern, the Archival End-State is confirmed. The shift does not appear as a price event. It appears as a structural change in participant logic. This change governs how capital allocates within the sector and which nodes receive priority in each new regime.

“This content is for informational and educational purposes only and does not constitute financial, investment, tax, or legal advice. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. Consult a qualified advisor before investing. Author may hold positions in discussed securities.”

Access Archive: Empirical Validation